The method of collecting payment is important for managing business cash-flow effectively. Here we look at a range of payment methods with their specific characteristics.

Cash

This includes bank credit transfers where the customer instructs their bank to send funds to a recipient bank account on a single occasion. With these payments, the customer has to explicitly authorise each transaction and businesses cannot use the payment details in the future.

Cheque

The use of cheques has reduced dramatically, being replaced by an increasing number of online transaction and electronic payment methods to pay for goods and services.

Money order payments

Best suited for business-to-business transactions when cash or cheques are not accepted. For those who do not have a chequebook, a money order payment is a substitute for a check.

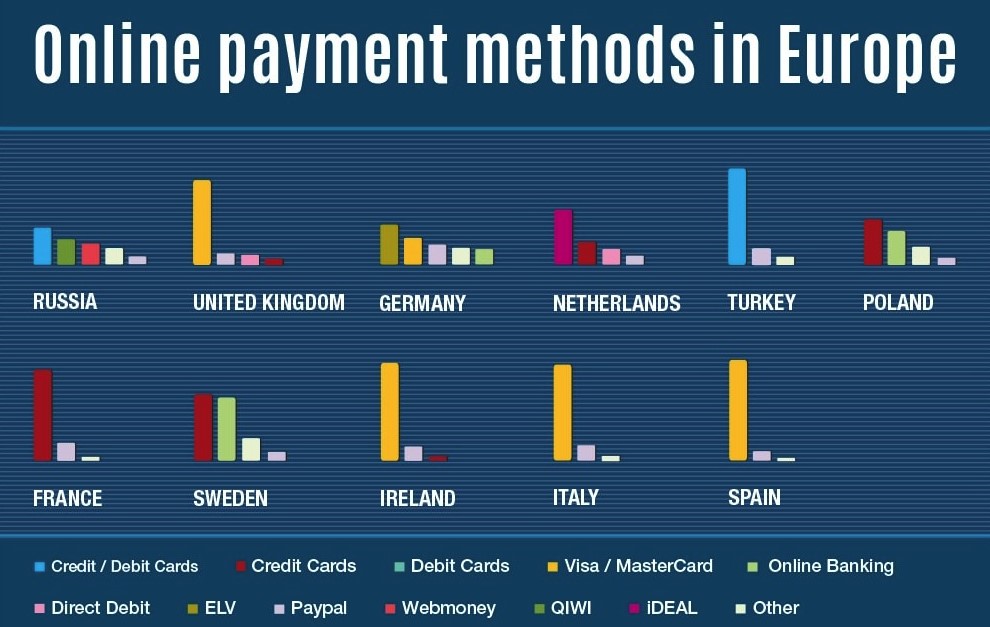

Credit and debit card payments

Credit and debit cards account for half the global online transactions. A business takes a risk accepting payment by credit card if they are unable to formally confirm that the card owner has authorised the transaction, or that the payment details have been provided by the card owner. A second stage security check reduces risk and liability.

Direct debit payments

A business is given permission by the customer to collect varying sums of money from their account when the sign a Direct Debit is an instruction.

Online payments

Online payments such as PayPal help businesses to diversify payment preferences through authenticated or irrevocable payment systems. Certain online payment methods only support payments in a limited number of currencies. Examples include iDEAL is a popular payment method in the Netherlands, Bancontact in Belgium, Klarna in Sweden, and China’s Alipay.

EFTPOS payments

Electronic funds transfer at point of sale (EFTPOS) is an electronic payment system using debit or credit cards at payment terminals located at points of sale. Systems are generally country specific and do not interconnect.

Gift cards and vouchers

Gift cards and vouchers, also known as gift certificates, are prepaid cards or tokens usually issued by a retailer to be used as an alternative to cash for purchases within a particular store or related businesses. Also used by businesses as a promotion strategy, to encourage return custom. Gift cards are usually only redeemable at particular retail premises and cannot be cashed out. Some cards have an expiry date.

Business credit

Retail companies with higher average order value transactions may consider offering a consumer credit payment option at checkout to increase conversions.

Bitcoin and digital currencies

Popular digital wallets are designed for individual consumers and offer limited support for large transaction amounts or business-to-business payments. Bitcoin payments are customer-initiated, with the customer given a particular address to send funds to. From a business view, Bitcoin and other digital currencies have the benefit of being irrevocable by customers.

How to choose a payment method

Cash is private and reliable, but is expensive to handle and has a higher risk of theft.

EFTPOS is fast, and the risk of theft is minimal. Costs include a phone line, electricity and service fees.

Credit cards automatically record transactions. Some customers might prefer to pay cash for certain goods and services, to keep this information private. Service fees may apply.

Subscriptions, as well as larger payments, can be settled by bank transfer, via direct debit or credit cards.